An income tax filing is not only about reporting one’s earnings but also about precision and timeliness, as any mistake can result in hefty fines, sometimes reaching as high as 200 per cent of the tax payable.

According to tax experts, there have been instances where people pay more tax than necessary because of avoidable errors in their returns. It is important for an individual to adopt a systematic approach and provide appropriate documentation to prevent such situations from arising.

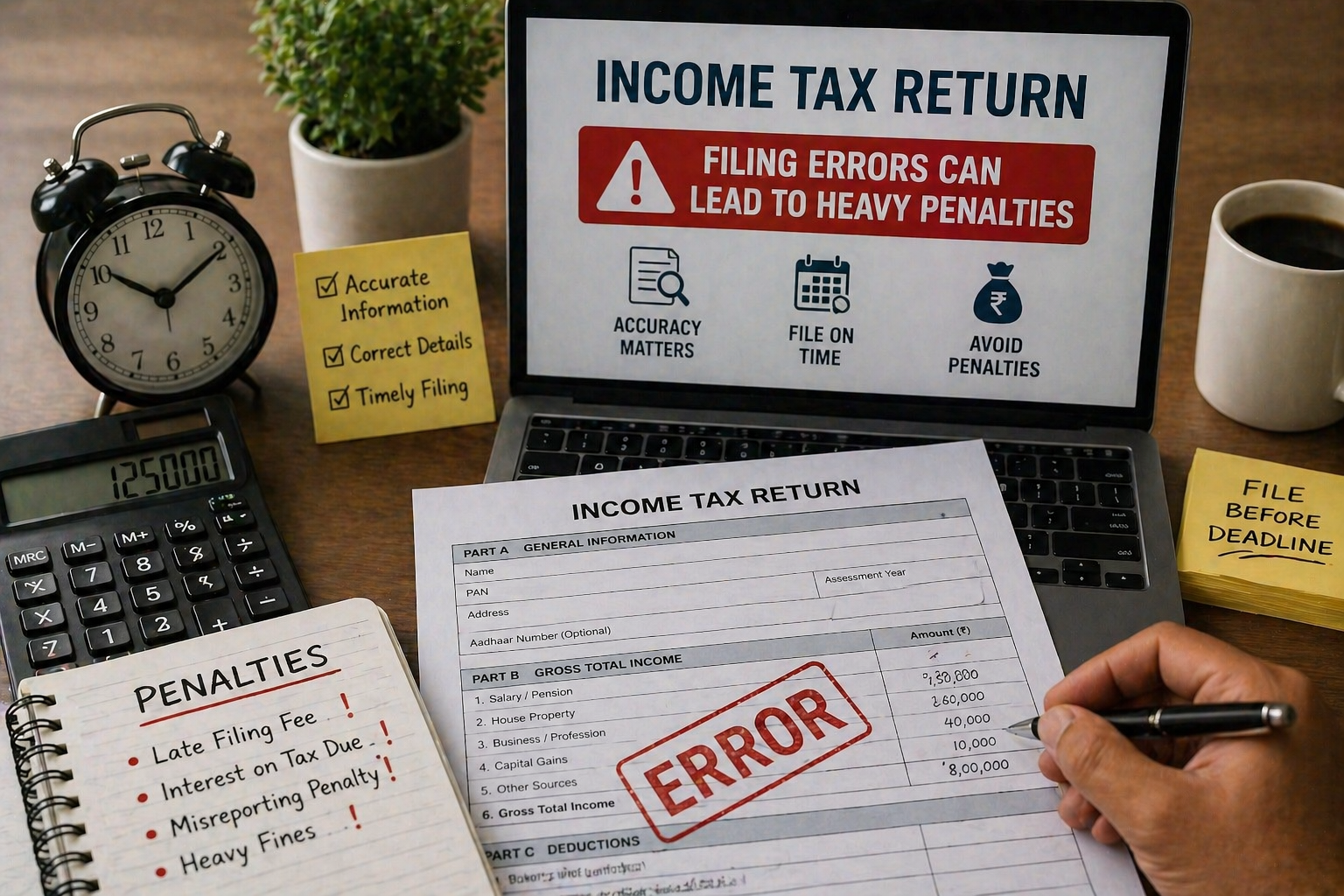

Common mistakes that can cost you

One of the most frequent triggers for tax notices is under-reporting or misreporting of income. Taxpayers often miss including income from bank interest, freelance work, capital gains, rental earnings or foreign assets.

Also Read | ‘Constructive but gaps remain’: Inside India-US trade talks in Washington

Authorities rely on tools such as the Annual Information Statement (AIS) and Form 26AS to cross-check disclosures. Any mismatch between these records and filed returns can lead to penalties.

Under Section 270A, under-reporting of income can attract a penalty of 50 per cent of the tax due, while deliberate misreporting can invite a penalty of up to 200 per cent.

Errors such as incorrect PAN details, wrong deduction claims or claiming exemptions without proof can also lead to complications.

Plan early, file carefully

Experts advise starting tax planning at the beginning of the financial year instead of rushing at the last minute. Common deductions under Sections 80C, 80D, 24(b) and 80CCD(1B) should be used based on individual financial goals, not just tax-saving intent.

“If tax is still due after TDS and advance tax, it must be paid before filing the return. Delays can lead to penalties and interest,” tax advisors told NDTV.

Also Read | New trouble for Paytm Payments Bank? RBI cancels license

Late filing itself can attract a fee of up to ₹5,000 under Section 234F.

Fix errors without delay

Taxpayers can make use of their right to file an amended tax return within the stipulated period. As per experts, any mistakes in the filing process must be corrected immediately, along with documentation proof such as investments, insurance, and loan details.

Chartered accountant Suresh Surana told NDTV, expenses involved in making investments for tax savings could lower the returns earned in the long run.

Taking time to check the paperwork before filing a tax return is the easiest thing that one can do.