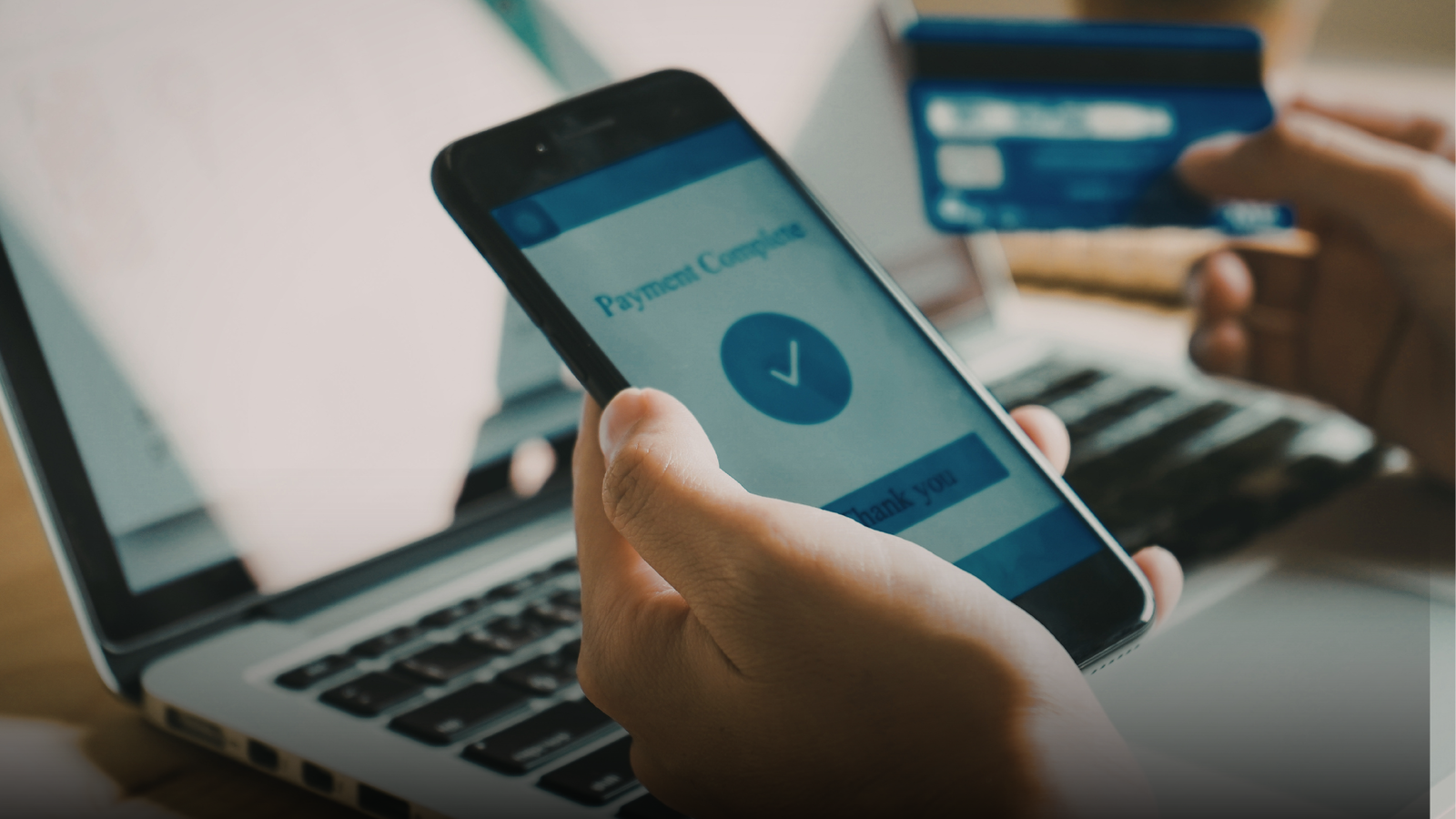

It is one of the most frequent UPI mistakes and, for many users, one of the most terrifying. You have just made a payment, and the “successful” notification pops up, only to realise a split second later that the amount has been sent to the wrong UPI handle. It may not be a large amount, but the fear is immediate since UPI is a real-time service and does not have an apparent “undo” button.

What happens next is usually less scary than users imagine and often less comforting than they hope for.

Why a successful UPI payment is difficult to undo

UPI transactions are designed to be instantaneous and irrevocable. This means that once the payment has been marked as successful, the amount has already been transferred from your bank account to the beneficiary’s account. There is no cooling-off period, as there would be with card transactions or failed bank transfers, and no automatic reversal of the transaction.

This is the bit that many users find difficult to grasp. Even if it is obvious that the transaction was a mistake, the banks cannot just reverse the transaction and take the money back. From a technical and legal perspective, the money is now in the recipient’s account. Any reversal of the transaction is now dependent on their consent.

This is a deliberate design choice. UPI prefers speed and surety over easy reversals, which puts the onus on the sender to check everything.

Also Read | Tired updating Aadhaar mobile number? UIDAI launches new App to simplify process

What the bank and the UPI app actually do

First, file a complaint through the UPI app that you used for the transaction. There is a dispute or “wrong transfer” option for every transaction that goes through. This will not reverse the funds but will initiate communication between the banks.

Then, your bank will contact the other bank, which will then notify the person who received the money that the transaction was wrong and ask for their permission to refund the money. If they agree, the money will be refunded in a few business days.

If the person does not respond or refuses, the banks have very little that they can do. Banks cannot withdraw money from an account without the account holder’s permission. In this case, you will be asked to file a complaint in writing or contact the police.

When money comes back automatically

There is one obvious situation where refunding money is easy: when the UPI ID you entered doesn’t exist, the transaction will likely fail, and the money will be refunded automatically. That’s why it is so important to check if the payment status is “successful” or “failed.”

If the payment is successful, the situation is now entirely in the hands of the receiver.

Also Read | Govt pilots hybrid ATMs to tackle small currency note crunch amid UPI push

Why acting quickly still matters

The sooner a complaint is raised, the better the chances of getting the money back. It will help you contact the receiver and will also indicate that the transaction was accidental. However, speed will not be able to waive the basic rule: banks do not have a time limit to reverse the transaction.

The reality of UPI mistakes

UPI is a clean system if handled carefully, but there is no room for mistakes. The only moment when the receiver’s name appears before you confirm the transaction is not just for show; it is the only safety net of the system.

After a transaction is completed, there is no way to reverse it.